Attorneys spend a surprising amount of time on the road. Between court appearances, depositions, client meetings, jail visits, and property inspections, a practicing lawyer can easily drive 10,000 to 20,000 business miles per year. Mileage tracking for lawyers serves a dual purpose: it reduces your tax bill and supports accurate client billing for travel expenses.

At the 2026 IRS standard mileage rate of 72.5 cents per mile, a trial attorney driving 15,000 business miles saves $10,875 on taxes. A family law attorney visiting clients and courthouses across multiple counties may save even more. The catch is that the IRS requires detailed, contemporaneous records for every trip.

What Driving Qualifies as Deductible for Attorneys

The IRS rules for business mileage apply to lawyers the same way they apply to any profession. The key distinction is between business travel and commuting.

Deductible business miles include driving from your office to the courthouse, travel to client meetings at their home or office, trips to depositions, mediations, and arbitrations, driving to the jail or detention center for client visits, travel to investigate a case or inspect property, trips to filing offices, banks, or the post office for firm business, and driving to continuing legal education seminars and bar events.

Non-deductible commuting is your regular drive from home to your office. However, if you maintain a qualifying home office as your principal place of business (common for solo practitioners), every trip from home to a work-related location becomes deductible.

Solo Practitioners vs Firm Employees

Your tax treatment depends on how your practice is structured.

Solo practitioners and firm owners who file as self-employed (Schedule C) or operate through an S-Corp can deduct business mileage directly. Self-employed attorneys claim the deduction on Schedule C. S-Corp owners receive tax-free reimbursement through an accountable plan, which is even more tax-efficient.

Associate attorneys and firm employees (W-2) cannot deduct unreimbursed mileage on their federal tax return. This deduction was permanently eliminated. If your firm does not reimburse driving expenses, you absorb the full cost.

If you are a W-2 attorney, check whether your firm has a mileage reimbursement policy. Many firms reimburse at the IRS rate for travel to courts, depositions, and client meetings. If yours does not, it may be worth raising the issue. For background on how employer reimbursement works, see our guide on mileage reimbursement for employees.

![]()

Billing Clients for Travel Mileage

Beyond tax deductions, mileage tracking helps lawyers bill clients accurately for travel expenses. Fee agreements and retainer letters often include provisions for travel reimbursement. Common billing approaches include the following.

IRS rate pass-through. Bill the client 72.5 cents per mile for travel to their matter-related locations. This rate is widely accepted as reasonable and is easy for clients to understand.

Hourly rate for travel time. Some attorneys bill their standard hourly rate (or a reduced rate) for time spent driving. If you charge $350 per hour and drive 45 minutes to a deposition, you bill $262.50 for travel time plus mileage costs.

Flat travel fee. Charge a predetermined amount per trip for clients beyond a certain distance. For example, $75 for any trip over 25 miles from the office.

Bundled into the case fee. For flat-fee matters, build estimated travel costs into the total fee. This works best for cases with predictable travel requirements.

Regardless of your billing approach, maintaining a precise mileage log with timestamps, destinations, and case references makes invoicing straightforward and defensible if a client questions the charges. Learn more about how to charge mileage to customers.

Creating an IRS-Compliant Mileage Log

The IRS requires “contemporaneous” mileage records for attorneys claiming the deduction. Your log must document the date of each trip, the starting point and destination, the business purpose (such as “hearing in Smith v. Jones, Case No. 2026-CV-1234”), and the total miles driven.

A log created from memory weeks or months after the fact does not satisfy the contemporaneous requirement. The IRS has denied mileage deductions in numerous cases where attorneys reconstructed logs from calendar entries at year-end.

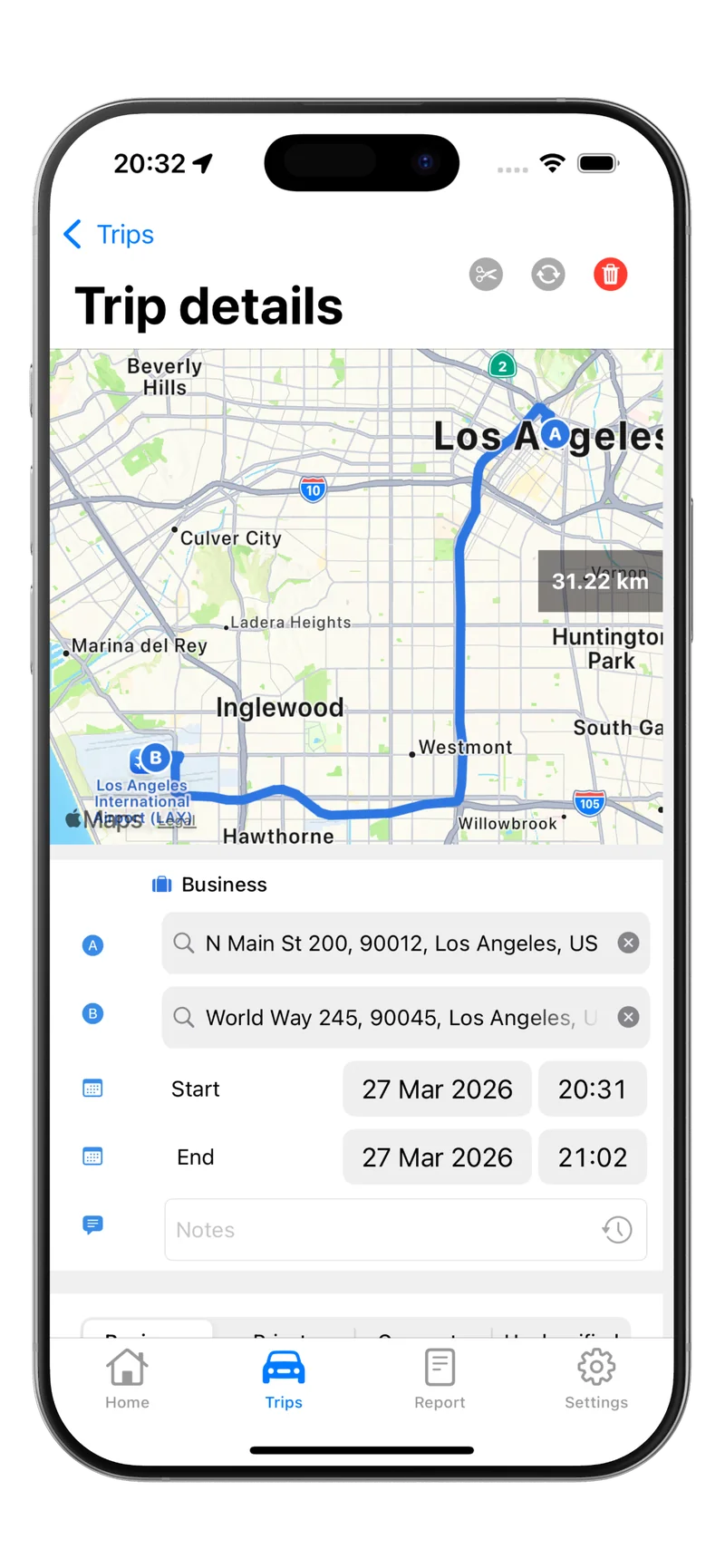

Tripbook automates this entire process. The app detects when you start driving and records the trip with GPS coordinates, route data, and precise mileage. After each trip, classify it as business with a swipe and add a case reference as a note. At billing time or tax time, export an IRS-compliant report.

![]()

Long-Distance Travel Deductions for Attorneys

Attorneys handling cases in distant courts or attending out-of-town depositions have additional deduction opportunities.

When you drive over 100 miles for a case-related trip, the mileage deduction still applies at 72.5 cents per mile. A round trip from your office to a courthouse 80 miles away generates a $116 deduction per visit.

For overnight business travel, you can also deduct lodging, 50 percent of meals, and incidental expenses in addition to mileage. Keep separate records for each category. The mileage deduction covers the vehicle costs; meals and lodging are tracked independently.

If you fly to a distant city and rent a car for case-related driving, the rental car costs and local mileage are both deductible as business travel expenses.

Ethical Considerations for Legal Mileage Billing

Bar ethics rules require attorneys to charge reasonable fees, and that includes travel-related charges. A few guidelines to keep billing defensible.

Be transparent in your fee agreement about how travel costs are calculated. Do not bill multiple clients for the same trip. If you attend a deposition for Client A and a meeting for Client B on the same route, allocate the mileage proportionally. Keep your mileage log accessible in case a client or the bar requests documentation.

Avoid double-dipping by billing a client for travel mileage while also claiming that mileage as a personal tax deduction when the client reimbursement fully covers the cost. If a client reimburses you for mileage, report the reimbursement as income and deduct the miles on your tax return, which nets out correctly.

Common Mistakes Attorneys Make With Mileage

Not tracking courthouse trips. A daily drive to the courthouse is one of the most common business miles lawyers incur. If you visit court three times per week, that adds up to 150 or more round trips per year.

Forgetting short errands. A quick trip to the filing office, a drive to pick up court documents, or a stop at the post office to mail a motion are all deductible. These 2 to 5 mile trips add hundreds of deductible miles annually.

Failing to separate personal detours. If you stop for lunch or run a personal errand during a business trip, the personal portion must be excluded from your deduction.

Not tracking mileage for pro bono work. Miles driven for pro bono cases are still deductible business miles if the work is part of your professional practice.

Every Legal Mile Counts

Mileage tracking for lawyers is both a tax reduction strategy and a client billing tool. Whether you are a solo practitioner claiming deductions on Schedule C or a firm partner billing clients for travel, accurate mileage records are essential. At 72.5 cents per mile, the deduction is too valuable to leave to guesswork.

Download Tripbook and start logging every courthouse visit, client meeting, and deposition drive automatically.