Insurance is a windshield profession. Between client visits, claims inspections, policy renewals, and prospecting calls, the average insurance agent drives 12,000 to 20,000 business miles every year. Effective mileage tracking for insurance agents turns all that driving into a tax deduction worth $8,700 to $14,500 annually at the 2026 IRS rate.

The catch? You only get that deduction if you keep a proper mileage log. Missing even 20% of your deductible trips could cost you $1,700 to $2,900 in lost write-offs. This guide breaks down exactly which miles qualify, how much you stand to save, and the fastest way to build a compliant log.

Why Insurance Agents Drive So Many Business Miles

Insurance is one of the most driving-intensive professions in the service industry. Unlike office-based jobs, your work happens at kitchen tables, job sites, and conference rooms across your territory.

A typical week might include five to eight client home visits, two or three claims inspections, a networking lunch, and a continuing education class. Each of those trips adds 15 to 40 miles round-trip to your odometer.

Agents covering rural territories drive even more. If your book of business spans multiple counties, 300 to 400 miles per week is common. Over 50 working weeks, that adds up to 15,000 to 20,000 miles a year, all of which are potentially deductible.

Which Miles Count as Business Miles for Insurance Agents

Not every mile you drive qualifies for the insurance agent mileage deduction. The IRS draws a clear line between business vs commuting miles, and getting it wrong can trigger audit problems.

These trips are deductible:

- Client home visits for quotes, reviews, and policy delivery

- Claims inspections and damage assessments

- Policy renewal meetings at a client’s home or office

- Prospecting and door-to-door canvassing

- Networking events, industry conferences, and CE courses

- Driving between appointments during the day

- Trips to the bank, post office, or office supply store for business needs

- Travel to meet with adjusters, underwriters, or agency staff at other locations

These trips are NOT deductible:

- Your daily commute from home to your main office

- Personal errands, even if they happen between business stops

- Driving to lunch unless it involves a business meeting

![]()

Home office tip: If you maintain a qualifying home office as your principal place of business, every trip from home to a client or business location becomes deductible. For most independent agents, this eliminates the commute exclusion entirely.

How Much Can You Save with the Mileage Deduction

The 2026 IRS standard mileage rate is 72.5 cents per mile. Here is what that looks like based on typical insurance agent driving patterns:

- 5,000 business miles/year: $3,625 deduction

- 10,000 business miles/year: $7,250 deduction

- 15,000 business miles/year: $10,875 deduction

- 20,000 business miles/year: $14,500 deduction

Those numbers represent the amount subtracted from your taxable income, not your actual tax refund. Your real tax savings depend on your bracket. An independent agent in the 22% federal bracket with 15,000 business miles saves roughly $2,393 in income tax plus $1,664 in self-employment tax, for a total of over $4,000 in real cash savings.

![]()

You can also add parking fees and tolls on top of your mileage deduction. Many agents overlook these, but they add up fast when you are visiting downtown clients or parking at hospital lots for claims meetings.

For a deeper walkthrough on the filing process, see our guide on claiming mileage deduction as a self-employed professional.

Independent vs Captive Agent Deduction Rules

Your ability to claim independent insurance agent tax deductions depends on how you are classified with the IRS.

Independent agents (1099 contractors): You file Schedule C and can deduct all business mileage using either the standard mileage rate or the actual expense method. Most independent agents choose the standard rate because it is simpler and often produces a larger deduction. You are also responsible for self-employment tax, which makes the mileage deduction even more valuable since it reduces both income and SE tax.

Captive agents (W-2 employees): Since the Tax Cuts and Jobs Act of 2018, W-2 employees can no longer deduct unreimbursed business expenses on their federal return. If your agency does not reimburse your mileage, you absorb that cost. The exception is if you live in a state that still allows unreimbursed employee expense deductions, such as California, New York, or Pennsylvania.

Statutory employees: Some insurance agents are classified as statutory employees (box 13 on your W-2 is checked). This is a special category that allows you to file Schedule C and deduct business expenses, including mileage, even though you receive a W-2. Check your pay stub or ask your agency if you are unsure.

Not sure about your status? Look at your year-end tax form. If you receive a 1099-NEC, you are an independent contractor. If you receive a W-2, check box 13 for statutory employee status. When in doubt, consult a tax professional.

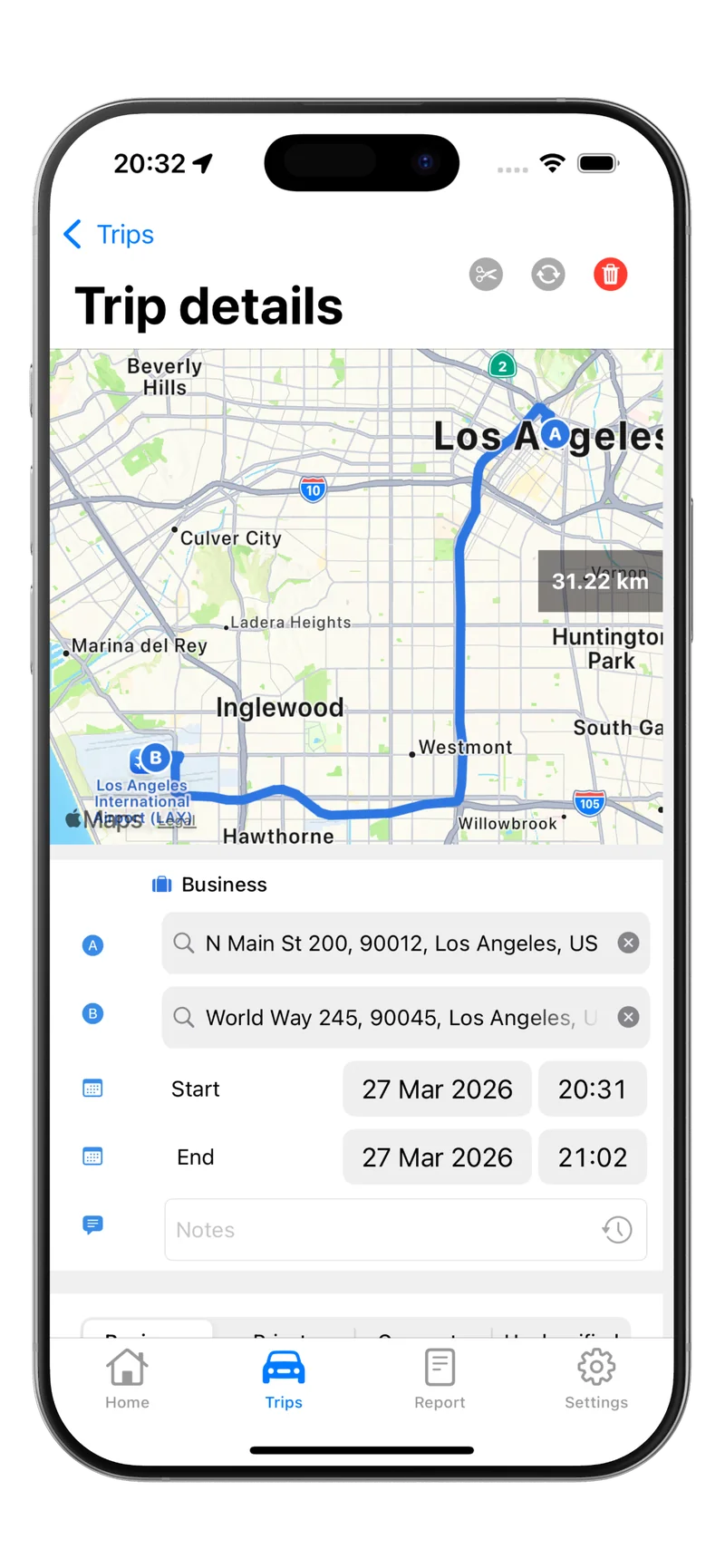

Mileage Tracking for Insurance Agents: The Easy Way

The IRS requires contemporaneous records for mileage deductions. That means you need to log each trip close to when it happens, not reconstruct your log at tax time. Every entry should include the date, starting location, destination, business purpose, and miles driven.

You have three options for building your mileage log:

1. Paper logbook: Cheap but unreliable. It is easy to forget trips, and handwritten logs are difficult to organize at year-end. Most agents who use paper logs miss 30% or more of their deductible miles.

2. Spreadsheet: Better than paper, but still requires manual entry after every trip. The friction means most agents stop updating it within a few weeks.

3. Automatic mileage tracking app: The most accurate and easiest method. Apps like Tripbook use your phone’s GPS and motion detection to record every trip automatically. You just swipe to classify each trip as business or personal, and the app builds an IRS-compliant log for you.

Automatic tracking captures trips you would otherwise forget, like the quick stop at a client’s house between two other appointments. Over a year, those forgotten trips add up to hundreds or even thousands of dollars in lost deductions.

With Tripbook, you can export your complete mileage log as a PDF, CSV, or XLS file whenever you need it. Reports include dates, addresses, mileage, and business purpose, which is exactly what the IRS wants to see during an audit.

If you work in another driving-heavy profession or want to see how other professionals approach this, check out our guide on mileage tracking by profession for real estate agents.

Start Tracking Every Deductible Mile Today

Insurance agents leave thousands of dollars on the table every year by not tracking their business miles consistently. Whether you drive 5,000 miles or 20,000 miles annually, the mileage deduction is one of the largest write-offs available to you.

Set up automatic tracking now so every client visit, claims inspection, and networking event gets logged without any effort on your part. Your future self will thank you at tax time.

Download Tripbook and start capturing every deductible mile from your very first trip.